字體:小 中 大

字體:小 中 大 |

|

|

|

| 2018/03/09 18:06:34瀏覽63|回應0|推薦0 | |

Infrastructure in IndiaInfrastrugglesOne of India’s most important industries has a knackered balance-sheetDec 31st 2011 | MUMBAI | from the print edition

ONE recent evening in Mumbai a tangerine Lamborghini could be seen taxiing past a sign prohibiting bullock carts, wheeling left and then letting rip on the Sea Link toll-bridge, one of the city’s few bits of decent infrastructure. For three miles all the driver’s Michael Schumacher fantasies must have came true. But by the fourth he drove off the bridge back into reality: roads whose surfaces often wash away during the monsoon and whose repair is said to be in the hands of mafias. The supercar returned to rickshaw speed. For the past half decade India’s infrastructure industry has enjoyed a Sea Link moment; a blast of growth when one could imagine that the private sector could deliver all the new roads, bridges, power stations and airports that the country needs so badly. The government says the boom will continue. Over the next five years it predicts that infrastructure investment will reach a new high relative to GDP, with some $1 trillion spent, half of it by the private sector. The trouble with this rosy prediction is that the balance-sheets of many Indian infrastructure firms are as potholed as the roads they resurface. In this section The backdrop is a slowing economy—growth has dipped below 7%—and a deep ditch of debt at infrastructure firms (which typically build, own or operate projects, or do a combination of the three, sometimes in partnership with the state). Government decision-making has slowed, partly due to drift at the top and because officials are scared of being accused of graft. All this has led to a “triple whammy” of distress, says Vinayak Chatterjee of Feedback Infra, a consultancy and engineering firm. First, new business has all but ground to a halt. Larsen & Toubro, one of the biggest infrastructure and engineering firms, saw a 2% quarter-on-quarter rise in its domestic order book at its last set of results. This is much less than it is used to. Money pits Second, cash flows are under strain. Firms get paid when they begin a project and when they reach milestones towards finishing it. Banks and investors are reluctant to hand over more funds. Finally there are worries about long-term profits. During the boom, firms bid recklessly for contracts (including an extension to the Sea Link bridge, won by the Reliance Group, run by Anil Ambani). With high interest rates and inflation a number of these deals may turn out to be duds. Some completed projects, including Delhi’s new airport, are losing money. The warning lights are flashing. But figuring out exactly what is going on is not easy. The industry is fond of financial engineering that has a whiff of subprime about it. Individual projects—for example an airport, power plant or stretch of road—are typically put in special-purpose vehicles which issue non-recourse debt. Infrastructure firms, which are often listed, have several kinds of links to these vehicles. In their accounts they may consolidate them on their balance-sheet, or, if they do not control them, treat them as investments. The result is dauntingly complex. Taking six big infrastructure firms’ disclosures in their annual reports, it is possible to find no fewer than 531 subsidiaries, joint ventures or associated entities. It gets more fiddly. Firms may lend money to projects they own no stake in and to contractors. They invite in minority investors at multiple levels in their holding structures, including private-equity funds that may use debt to finance their purchases. And overlaying all this is sloppy disclosure and a habit of focusing on firms’ “stand-alone” accounts. Roughly speaking, these try to capture the core business, pretty much as defined by the managers, rather than the “consolidated” accounts which try to include all subsidiaries and investments, warts and all, and which are the accounting benchmark globally.

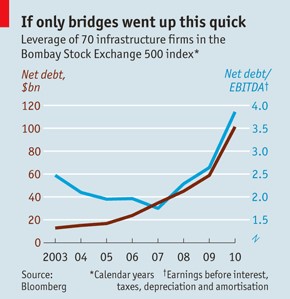

Those consolidated figures are at least published annually (and more frequently by some noble firms) and are the best guide to what is going on. Take 70 or so listed infrastructure firms from the BSE-500 index, broadly defined to include power, telecoms, construction and asset owners, and the effects of the boom are plain to see. Leverage has risen dramatically (see chart). Just over half of these firms had ratios of net debt to gross operating profits (or “EBITDA”) of over three times last financial year, and/or have net debts in excess of their current market value, two rules of thumb to identify knackered balance-sheets. Thanks to heavy investment, the 70-odd firms were cashflow-negative (defined as EBITDA less capital expenditure) to the tune of $12 billion. Assuming a 12% interest rate, their accounting operating profits last year only just exceeded their interest costs.

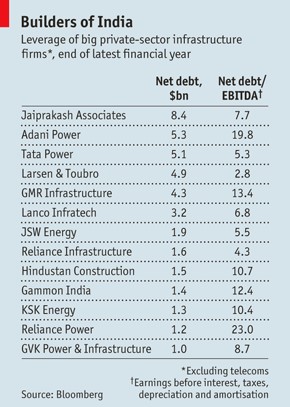

Exclude state-owned and telecoms firms and leverage is worse (see table). From public disclosures it is impossible to work out the liquidity position of these firms, but it is likely that most will have to refinance existing credit lines in today’s far less forgiving world, a process not helped by high local rates and a weak rupee. It looks like a mess. Shareholders have taken a beating, with the market value of those 70-odd stocks having fallen by some two-fifths since March 2011. India’s banks may be next in line for a thrashing. The Reserve Bank of India (RBI), the regulator, reckons they have 13% of their loan book in infrastructure (vaguely reassuringly, the RBI’s implied absolutedebt figure roughly matches the $130 billion of gross debt of the 70 listed firms). Thus far non-performing loans are low—so low it suggests banks are fibbing. But the RBI is probably right that a rickety infrastructure sector does not endanger the banking system. What it does endanger is India’s growth prospects. Those new airports, roads and bridges are essential. And the country does not need financial zombies, slashing their investment in order to shore up dodgy balance-sheets. Some reckon the solution is to develop a bond market, so that more debt can be raised. But while a more sophisticated capital market might mean more funds available and might even reduce the amount of financial engineering going on, it is not the solution to today’s predicament. Instead, two things need to happen. The government needs to unsnarl stalled projects. And infrastructure firms need to raise lots more equity—not debt. That might dilute the stakes which are held by some of the magnates who control these businesses, but would be a fair price to pay to resuscitate the balance-sheet of a vital industry. Even on selfish grounds it makes sense, hastening the day when an honest Indian oligarch can at last put the pedal to metal in his supercar for more than three miles in a row. from the print edition | Business

Infrastruggles Dec 29th 2011, 14:49

For India, keeping the quality of infrastructure is really a very big issue, especially facing the multiple situation in this elephant country. One of points to predict the vision of investment in a country is to measure the degree of infrastructure’s maturity.

Among the BRIC’s aggressive competiton, the only catogory India wins over other three is infrastructure. Especially comparing with China, India cannot take any grade but which of infrastructure to say India has the ability to attract foreign direct investment (FDI). If there is another reason, that is the Oxford doctor degree of prime minister Manmohan Singh higher than which of China’s communist party’s Hu Jing-Tao, Wen Jia-Bao and the next leader Xi Jin-Ping, Li Ke-Qiang.

With the recover of world economy, many developed countries regain their focuses on these four countries. According to yesterday’s NHK world, Japan’s prime minister Yoshihiko Noda is visiting New Delhi to meet Mr. Singh couple by the end of this year after his visit to Beijing to talk with China’s President Hu Jing-Tao and prime minister Wen Jia-Bao, saying Japan is ready to provide assistance to Indian infrastructure projects. Mr. Noda indicates that the 2 countries share these clear and mutually complementary economic conditions, beyond their obvious relationship, showing very friendly relation with India. But on one side, there is just some worse shortage concerned of infrastructure in China than in Beijing. Throwing mass investment to China better than to India is indeed worth getting better benefit successfully. On the other side, Mr. Noda changed the day he met China’s Hu and Wen, making many people connect the 1941’s Nanjing Massacre and this visit (because of the same date) either deliberately or to no purpose.

As the author referred to the airport, roads and bridges, the economic growth is depending on the infrastructure very much. However, although India can sustain more than 7% high economic growth in 5 years, India has serious inflation problem on consumer price index(CPI). For more than two years, India has been facing more than 5% per one month terrible CPI rapid increase. Mr. Singh and his successor Rahul Gandhi, India’s incumbent president Sonia Gandhi’s son, seem not to provide the solution to this serious inflation problem. Therefore, it’s hard to know whether this elephant can show more magic in front of the world.

Recommended 30 Report Permalink 筆者根據當時的NHK World報導印度當地的民情,普遍無感於國大黨的解決基礎建設的新方法,雖然人才輩出,仍然仰賴中國和日本的技術,當時近日來有日本野田首相及中國的胡錦濤、溫家寶和印度辛格前總理交流時均提及議題,希望能創造雙贏。印度當時是個三高:高血壓、高血糖、高血脂。經濟成長快速(GDP 成長率growth rate)依靠高通貨膨脹(CPI)和高失業人口,且文盲問題在衛星都市是國際間城鄉開發議題中最嚴重的。當年的印度是個講究重視個人成就及尊重個人自由的國度,所以比頭腦者,去個孟買或新德里才半年一年就晉身富豪者不在少數,同時高風險也有一天賠掉當時的半間鴻海的事的。雖說打腫臉充胖子就國大黨最後十年算是成功吸引外資,以及配合像Bangalore 班加羅爾的成功經驗,但仍稍嫌不足,不知穩健經濟、何談穩定民生,最後較親本土化的印度人民黨及其聯盟獲勝執政。 |

|

| ( 心情隨筆|心情日記 ) |